The New Power Grid

How AI's Energy Demands are Reshaping the Global Energy Market

The rapid and exponential growth of artificial intelligence (AI) has triggered an unprecedented surge in demand for computational power, and consequently, for the energy required to fuel it. This paper provides a comprehensive analysis of the profound impact of AI’s burgeoning energy consumption on the global energy market. It examines the current and projected energy needs of AI data centers, which are expected to more than double by 2030, and evaluates the viability of various power sources—including nuclear, natural gas, solar, wind, geothermal, and hydroelectric—to meet this demand. The paper explores the strategic responses of major technology corporations, which are increasingly entering into long-term power purchase agreements (PPAs) for nuclear and renewable energy, and even investing in the development of new energy infrastructure. Furthermore, it delves into the significant challenges facing the existing power grid, the critical role of energy storage solutions, and the evolving policy and regulatory landscape. The analysis concludes by highlighting the critical assumptions and uncertainties that could shape the future of AI’s energy consumption, ultimately arguing that a diversified, resilient, and intelligent energy strategy is paramount to sustainably power the AI revolution.

1. Introduction

The 21st century is being defined by the rise of artificial intelligence. From a niche academic pursuit, AI has evolved into a transformative general-purpose technology, poised to reshape industries, economies, and societies. However, this revolution is built on a foundation of immense computational power, and that power requires a staggering amount of energy. The proliferation of large language models (LLMs), generative AI, and other advanced AI applications has created a new and voracious consumer in the global energy market: the AI data center.

This paper examines the escalating energy demands of AI and the consequential shifts in the energy sector. It seeks to answer a critical question: how will the world power the future of artificial intelligence? To do so, this paper will first quantify the scale of AI’s energy consumption, drawing on recent projections from leading energy and financial institutions. It will then provide an in-depth analysis of the primary energy sources vying to meet this demand, evaluating their respective strengths, weaknesses, and strategic importance. The paper will also explore the critical role of grid infrastructure and energy storage in ensuring a stable and reliable power supply. Finally, it will analyze the strategic maneuvers of key industry players and the evolving policy landscape that will ultimately determine the energy future of AI.

2. The Unprecedented Growth of AI Energy Demand

The energy consumption of data centers is not a new phenomenon, but the advent of AI has introduced a new dimension to the challenge. AI workloads, particularly the training of large models, are significantly more energy-intensive than traditional computing tasks. This has led to a dramatic increase in the power density of data centers and a surge in their overall energy consumption.

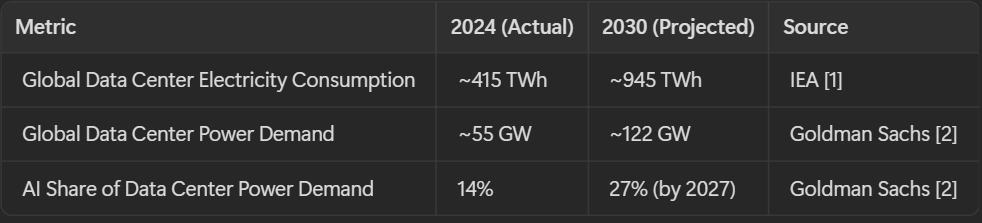

According to the International Energy Agency (IEA), global data center electricity consumption is projected to more than double from approximately 415 TWh in 2024 to around 945 TWh by 2030, a compound annual growth rate of about 15% [1]. To put this in perspective, the projected 2030 consumption is roughly equivalent to the current annual electricity consumption of Japan. Goldman Sachs Research offers an even more aggressive forecast, predicting a 165% increase in data center power demand by the end of the decade [2].

This growth is not evenly distributed. The IEA notes that while conventional servers are projected to see a 9% annual growth in electricity consumption, accelerated servers, which are primarily used for AI, are expected to grow at a staggering 30% annually [1]. This disparity underscores the central role of AI in driving the surge in data center energy demand.

This exponential growth in energy demand presents a formidable challenge to the global energy system, which is already grappling with the transition to a low-carbon future. The following sections will explore the various energy sources that are being considered to meet this challenge.

3. Analyzing the Contenders: A Deep Dive into Energy Sources

The quest to power the AI revolution has ignited a new debate about the future of energy. While renewable energy sources like solar and wind have been the focus of decarbonization efforts, their intermittent nature poses a challenge for data centers that require a constant, 24/7 power supply. This has led to a renewed interest in baseload power sources, particularly nuclear energy, and a pragmatic reliance on natural gas as a bridging fuel. This section provides a detailed analysis of the main contenders in the race to power AI.

3.1. Nuclear Power: The Resurgent Giant

Once considered a relic of the 20th century, nuclear power is experiencing a remarkable resurgence, driven in large part by the energy demands of AI. Nuclear power offers a unique combination of carbon-free, baseload electricity, making it an attractive option for powering data centers that require a constant and reliable energy supply.

The U.S. Department of Energy (DOE) has highlighted several advantages of nuclear power for data centers, including its 24/7 power generation, high reliability, and long operational cycles [3]. Modern nuclear plants can operate for 18 to 24 months without refueling, and advanced reactor designs are targeting operational cycles of up to 10 years. This level of reliability is a perfect match for the

99.999%+ uptime requirements of modern data centers.

Furthermore, the development of Small Modular Reactors (SMRs) and microreactors offers a new level of flexibility and scalability. These smaller, factory-built reactors can be deployed more quickly and at a lower cost than traditional large-scale nuclear plants, and their compact footprint makes them ideal for co-location with data centers, reducing transmission costs and increasing energy efficiency. The global pipeline for SMR projects reached 47 GW by the first quarter of 2025, with over half of that capacity in the United States, indicating a significant industry shift [4].

This potential has not gone unnoticed by the tech giants at the forefront of the AI revolution. In a series of landmark deals, major hyperscalers have made significant commitments to nuclear power:

•Microsoft entered into a 20-year Power Purchase Agreement (PPA) with Constellation Energy to support the restart of the Three Mile Island Unit 1 nuclear plant [3].

•Google has partnered with Kairos Power to develop up to 500 MW of SMR capacity, with the first reactors expected to come online in 2030 [4].

•Amazon has made multiple commitments, including a $650 million deal with Talen Energy for up to 960 MW of power from the Susquehanna nuclear plant and a separate agreement to purchase 1.9 GW of power from the same facility through 2042 [4].

•Meta (formerly Facebook) signed a 20-year PPA with Constellation Energy for 1.1 GW of nuclear energy from the Clinton Clean Energy Center in Illinois [4].

These strategic investments signal a growing recognition that nuclear power will be a critical component of the future energy mix for AI. However, significant challenges remain. The high upfront capital costs of nuclear power plants, the lengthy construction and licensing timelines, and the unresolved issue of long-term nuclear waste storage are all significant hurdles that must be overcome. Additionally, the regulatory landscape for new nuclear technologies, particularly SMRs, is still evolving.

3.2. Natural Gas: The Pragmatic Bridge

While nuclear power holds immense long-term promise, its deployment at the scale required to meet AI’s energy demands will take time. In the interim, natural gas has emerged as the pragmatic bridging fuel, offering a reliable and dispatchable source of power that can be deployed much more quickly than nuclear.

Natural gas power plants can be ramped up and down within minutes, making them ideal for balancing the grid and responding to fluctuations in energy demand. They can also operate at high capacity factors, providing the kind of reliable baseload power that data centers require. The United States, as the world’s largest producer of natural gas, is particularly well-positioned to leverage this resource to power its burgeoning AI industry [5].

In response to the surge in data center development, utilities in key markets like Virginia, Georgia, and the Carolinas have announced plans to add a combined 20 GW of new natural gas generation capacity by 2040 [5]. This trend is not without controversy, as it raises concerns about locking in fossil fuel infrastructure for decades to come and potentially undermining climate goals. However, from the perspective of data center operators, the immediate need for reliable power often outweighs these long-term concerns.

An interesting development in this space is the rise of off-grid natural gas solutions. Faced with grid connection delays and transmission constraints, some data center developers are bypassing the grid altogether and building their own dedicated natural gas power plants. This trend is particularly prevalent in Texas, where a combination of abundant natural gas resources, a favorable regulatory environment, and tax advantages have created a fertile ground for off-grid AI data centers [5]. For example, CloudBurst has a 10-year agreement with Energy Transfer to power a 1.2 GW data center, and major players like ExxonMobil and Chevron are now entering the space to develop dispatchable power plants specifically for data centers.

3.3. Renewables and the Storage Imperative

Renewable energy sources, particularly solar and wind, are the cornerstone of global decarbonization efforts and play a significant role in the energy strategies of major tech companies. Hyperscalers are the largest corporate buyers of renewable energy, and data centers already account for half of all corporate clean energy procurement in the United States [6]. The IEA projects that renewables will meet nearly 50% of the growth in data center electricity demand through 2030 [7].

However, the intermittent nature of solar and wind power presents a fundamental challenge for data centers that require an uninterrupted power supply. The sun doesn’t always shine, and the wind doesn’t always blow, creating a mismatch between energy generation and demand. This has made energy storage a critical enabling technology for integrating renewables into the data center power mix.

Battery Energy Storage Systems (BESS) are emerging as a key solution to this challenge. BESS can store excess renewable energy when it is abundant and discharge it when it is needed, providing a buffer against the intermittency of solar and wind power. In some cases, batteries are even being used to accelerate data center deployment by providing a temporary power source while waiting for grid connections. Aligned Data Centers, for example, is building a 31 MW battery to get a new facility online faster [8].

Beyond lithium-ion batteries, other storage technologies are also gaining traction. Flow batteries and zinc batteries offer the potential for longer-duration storage, which will be crucial for ensuring grid stability as the penetration of renewables increases. The market for energy storage solutions for data centers is expected to grow significantly, with some analysts predicting a $50 billion opportunity in the coming years [9].

3.4. Geothermal and Hydroelectric: The Unsung Heroes

While nuclear, natural gas, and solar/wind dominate the headlines, geothermal and hydroelectric power are also playing an important, albeit more geographically constrained, role in powering the AI revolution.

Geothermal energy taps into the Earth’s natural heat to generate electricity, offering a source of 24/7, carbon-free baseload power. The development of Enhanced Geothermal Systems (EGS) is expanding the geographic potential of this resource, and companies like Fervo Energy are developing geothermal-powered data center corridors [10]. Meta has also partnered with Sage Geothermal to power its data centers. Like nuclear, geothermal offers the reliability that data centers crave, but its deployment is limited to areas with suitable geological conditions.

Hydroelectric power is another source of clean, reliable baseload power that has long been a part of the energy mix. Data centers in regions with abundant hydropower resources, such as the Pacific Northwest and parts of Canada and Scandinavia, have been able to take advantage of this low-cost, carbon-free energy source. Google, for instance, has a 3,000 MW hydro deal with Brookfield to power its data centers [11]. However, the potential for new large-scale hydroelectric projects is limited, as most of the world’s most suitable sites have already been developed.

4. Navigating the Bottlenecks: Grid Infrastructure and Policy

The rapid growth of AI data centers is placing immense strain on the world’s aging electrical grids. The sheer scale of the new demand, coupled with its concentrated nature, is creating bottlenecks that threaten to derail the AI revolution. Data centers are being built faster than the generation and transmission infrastructure needed to power them, leading to long grid connection queues and delaying the integration of new energy projects.

This has triggered a flurry of policy and regulatory activity aimed at streamlining the permitting process and accelerating the buildout of new energy infrastructure. In the United States, the Trump administration issued an executive order in July 2025 to fast-track the permitting of AI data centers and supporting infrastructure [12]. The Department of Energy has also directed the Federal Energy Regulatory Commission (FERC) to accelerate its review process for large load interconnections [13].

However, these efforts are not without their challenges. There are complex regulatory issues to navigate, particularly around cost allocation for grid upgrades and the potential for data center demand to drive up electricity prices for other consumers. At the state level, policymakers are grappling with how to balance the economic benefits of data center development with the need to protect ratepayers and meet climate goals [14].

5. The Road Ahead: Critical Assumptions and Uncertainties

The future trajectory of AI’s energy consumption is subject to a high degree of uncertainty. The projections cited in this paper are based on a set of assumptions that may or may not hold true. The IEA, in its analysis, highlights several key uncertainties, including the rate of AI adoption, the pace of efficiency improvements in AI hardware and software, and the potential for energy sector bottlenecks to constrain growth [15].

For example, significant improvements in the energy efficiency of AI chips and algorithms could moderate the growth in energy demand. Conversely, the development of even more powerful and energy-intensive AI models could accelerate it. The economic viability of various energy sources will also play a crucial role. If the cost of SMRs comes down faster than expected, nuclear power could play an even larger role. If breakthroughs in energy storage technology make renewables more reliable and cost-effective, they could capture a larger share of the market.

Ultimately, the future of AI and energy will be shaped by a complex interplay of technological innovation, market forces, and policy decisions. The only certainty is that the demand for energy to power AI will continue to grow, and the energy market will have to adapt to meet this challenge.

6. Conclusion

The emergence of AI as a major energy consumer is a transformative event for the global energy market. The sheer scale and relentless growth of AI’s power demands are forcing a fundamental rethinking of our energy infrastructure, investment strategies, and policy priorities. The race to power AI is not simply about building more power plants; it is about building a new kind of power grid—one that is more intelligent, more resilient, and more diverse than ever before.

Our analysis suggests that there will be no single winner in this race. The future energy mix for AI will be a diversified portfolio of technologies, with nuclear power and natural gas providing the baseload reliability that data centers require, and renewables, paired with energy storage, offering a clean and increasingly cost-effective source of power. Geothermal and hydroelectric power will also play important roles in regions where they are available.

For the tech giants at the forefront of the AI revolution, the challenge is clear: they must become not just consumers of energy, but also active participants in the energy market, investing in new technologies, forging strategic partnerships, and advocating for policies that will ensure a sustainable and reliable energy future. For policymakers and energy providers, the challenge is to create a regulatory and market environment that can accommodate the rapid growth of AI while ensuring a just and equitable energy transition for all.

The road ahead is fraught with challenges, but it is also filled with opportunity. The same AI technologies that are driving this surge in energy demand can also be used to create a more efficient, intelligent, and sustainable energy system. By harnessing the power of AI to optimize our grids, accelerate the development of new energy technologies, and improve our energy efficiency, we can ensure that the AI revolution is not just a technological one, but also a sustainable one.

References

[1] International Energy Agency. (2025). Energy and AI. https://www.iea.org/reports/energy-and-ai/energy-demand-from-ai [2] Goldman Sachs. (2025). AI to drive 165% increase in data center power demand by 2030. https://www.goldmansachs.com/insights/articles/ai-to-drive-165-increase-in-data-center-power-demand-by-2030 [3] U.S. Department of Energy. (2025). Advantages and Challenges of Nuclear-Powered Data Centers. https://www.energy.gov/ne/articles/advantages-and-challenges-nuclear-powered-data-centers [4] Trellis. (2025). Amazon, Google, Meta and Microsoft go nuclear. https://trellis.net/article/amazon-google-meta-and-microsoft-go-nuclear/ [5] Data Center Dynamics. (2025). How natural gas is powering the US AI data center boom. https://www.datacenterdynamics.com/en/analysis/welcome-to-gas-land-how-natural-gas-is-powering-the-us-ai-boom/ [6] S&P Global. (2024). Data centers account for half of US clean energy procurement, but only 20% in Europe: report. https://www.spglobal.com/commodity-insights/en/news-research/latest-news/electric-power/103124-data-centers-account-for-half-of-us-clean-energy-procurement-but-only-20-in-europe-report [7] International Energy Agency. (2025). Energy supply for AI. https://www.iea.org/reports/energy-and-ai/energy-supply-for-ai [8] Canary Media. (2025). In a first, a data center is using a big battery to…. https://www.canarymedia.com/articles/batteries/aligned-data-center-get-online-faster [9] InvestorPlace. (2025). The Coming AI Energy Crunch – and the $50-Billion Opportunity No One Sees Yet. https://investorplace.com/hypergrowthinvesting/2025/10/the-coming-ai-energy-crunch-and-the-50-billion-opportunity-no-one-sees-yet/ [10] Fervo Energy. (2025). The Enhanced Geothermal Data Center Corridor. https://fervoenergy.com/fervo-uipa-the-enhanced-geothermal-data-center-corridor-july-2025/ [11] Data Centre Magazine. (2025). Google Taps Hydro Power to Fuel Data Centre Expansion. https://datacentremagazine.com/news/google-brookfield-launches-3-000-mw-hydropower-partnership [12] The White House. (2025). Accelerating Federal Permitting of Data Center Infrastructure. https://www.whitehouse.gov/presidential-actions/2025/07/accelerating-federal-permitting-of-data-center-infrastructure/ [13] Reuters. (2025). US pushes regulators on connecting data centers to grid. https://www.reuters.com/business/energy/us-pushes-regulators-connecting-data-centers-grid-2025-10-24/ [14] National Caucus of Environmental Legislators. (2025). States Act to Align Data Center Energy Demand with Climate Goals. https://www.ncel.net/articles/states-act-to-align-data-center-energy-demand-with-climate-goals/ [15] International Energy Agency. (2025). Executive summary – Energy and AI. https://www.iea.org/reports/energy-and-ai/executive-summary

The AI datacenter energy crunch is exactly why companes like OKLO are positioning themselves for rapid growth. The analysis on doubling energy needs by 2030 aligns with their SMR deployment timline. Nuclear makes sense for baseload requirments but the real question is wheher modular reactors can scale fast enough.